Why Does USCIS Review the Source of Funds?

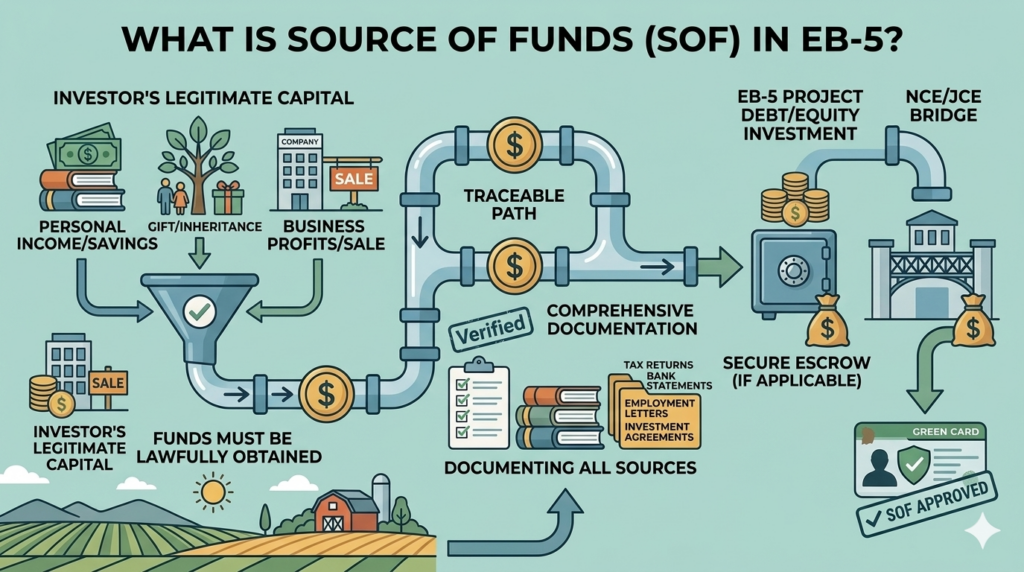

EB-5 is an investment-based immigration program, but the investment capital cannot come from unidentified or unlawful activity.

USCIS therefore reviews whether the investor obtained the money lawfully. This review helps determine whether the investor personally qualifies for EB-5 classification.

For example, an investor may have $800,000 available in a bank account. However, if the records do not explain where the money came from, USCIS may ask further questions.

The balance alone does not prove the source.

The investor may need to show that the capital came from years of employment income, a business distribution, a property sale, a gift from parents, or another lawful event. USCIS reviews each investor’s lawful source of funds as an individual eligibility issue, even when the investor is joining a project that has already received project-level approval.

This is why a strong EB-5 project cannot solve a weak personal source-of-funds case. The project and the investor are reviewed separately.

Source of Funds and Path of Funds Are Not the Same

Investors often hear the terms source of funds and path of funds used together. They are closely related, but they describe different parts of the financial story.

The source of funds explains where the money originally came from.

The path of funds explains how the money moved from that original source to the EB-5 investment account.

For example, imagine that an investor sells an apartment and uses the proceeds for EB-5.

The apartment sale is the source of funds. The investor may need to show ownership of the property, the sale agreement, the sale price, taxes, and receipt of the proceeds.

If the sale proceeds then move through several bank accounts before reaching the EB-5 project, those transfers form the path of funds.

A complete case should answer both questions:

- How was the capital lawfully obtained?

- How did that capital reach the EB-5 investment?

In my experience, many source-of-funds problems are actually path-of-funds problems. The original income may be perfectly lawful, but one or more transfers are missing from the records.

Common Lawful Sources of EB-5 Funds

There is no single required source of EB-5 capital. Investors may rely on one source or combine several sources, depending on their circumstances.

Employment Income and Savings

An investor may use salary, bonuses, or savings accumulated over many years.

In this type of case, USCIS may need to understand the investor’s employment history, annual income, taxes, living expenses, and how the savings accumulated.

The difficulty is often not proving that the investor had a good job. The difficulty is showing that the income was sufficient to support the amount being invested.

Business Profits or Dividends

Business owners may use company profits, distributions, or dividends.

The investor may need to show ownership of the business, the company’s lawful operations, its financial performance, its ability to make the distribution, and the transfer into the investor’s personal account.

A company payment should not appear in the bank account without a clear explanation of why the investor was entitled to receive it.

Property Sale Proceeds

Many investors use proceeds from selling residential or commercial property.

This may require evidence of ownership, purchase history, the sale transaction, taxes, and receipt of the proceeds.

Sometimes the property was purchased many years ago, and the original documents are difficult to obtain. In that situation, the attorney may need to build the best possible record using available primary and secondary evidence.

Gifts

Parents frequently gift EB-5 funds to an adult child, particularly when the child is the principal investor.

A gift can be a lawful source, but USCIS will generally look beyond the transfer itself. The donor may need to prove how they lawfully obtained the gifted money.

The investor should also show that the transfer was a genuine gift rather than an undisclosed loan that must be repaid. Current Form I-526E instructions specifically address gifted and loaned funds and require supporting evidence concerning the donor or lender and the legitimacy of the transfer.

Loans

Loan proceeds may be used in an EB-5 case when properly structured and documented.

The investor may need to establish the loan terms, the identity of the lender, any collateral involved, the investor’s repayment obligation, and the lawful source of the lender’s money.

A bank loan secured by the investor’s own property may look very different from a private loan from a relative. Each structure requires its own analysis.

Inheritance

Inherited funds may also qualify as a lawful source.

The investor may use estate documents, a will, probate records, death certificates, bank records, tax documents, and evidence showing how the inherited assets were transferred.

Older inheritances may require additional explanation when formal records are incomplete.

Can You Combine Several Sources?

Yes. An investor may use more than one lawful source.

For example, the investment could be funded through:

- $300,000 from salary savings;

- $300,000 from a property sale; and

- $200,000 as a gift from a parent.

However, each portion must be documented separately. Combining several sources may be completely acceptable, but it usually increases the number of documents and transactions that must be explained.

This is why the simplest funding structure is not always the one involving the fewest accounts. It is the one with the clearest evidence.

What About the Administrative Fee?

Investors often focus only on documenting the required investment capital and overlook the project administrative fee.

The administrative fee may also need a lawful and traceable funding explanation. The Form I-526E instructions ask investors to identify the sources of capital invested in the new commercial enterprise as well as funds used to pay certain costs and fees associated with the investment.

For this reason, investors should not assume that only the main investment transfer matters. The entire transaction should be reviewed with the immigration attorney before funds are moved.

What USCIS Is Really Looking For

In my experience, investors often believe they need to produce the largest possible number of documents. But quantity alone does not make a strong source-of-funds case.

USCIS is trying to understand a financial story.

That story should show:

- Who earned or owned the money;

- How it was lawfully acquired;

- Where it was held;

- Why it was transferred;

- Who controlled each account;

- Whether any donor or lender was involved; and

- How the money reached the EB-5 investment.

The documents should support one consistent explanation. Names, dates, amounts, ownership details, and account records should match.

When the reviewer can follow the financial story without having to fill in major gaps, the case is usually much easier to understand.

Common Misunderstandings

One common misunderstanding is that wealthy investors do not need detailed documentation. In reality, a high net worth does not replace source-of-funds evidence.

Another misunderstanding is that funds already sitting in a U.S. bank account are automatically acceptable. The location of the account does not establish how the funds were earned.

Investors may also assume that a gift solves documentation problems. It does not. A gift usually moves the source-of-funds review to the donor.

Finally, some investors believe that older transactions no longer matter. But if an old transaction explains how the investment capital was created, USCIS may still want supporting evidence.