When investors first come to me to discuss EB-5, many of them already have a project brochure in hand. They may have heard that one project is “safe,” another project is “fast,” or another project has “already been approved.” Some have watched videos online. Some have spoken with agents. Some have friends who already invested.

But after working in this industry for many years, I have learned that most investors should take one step back before making any decision.

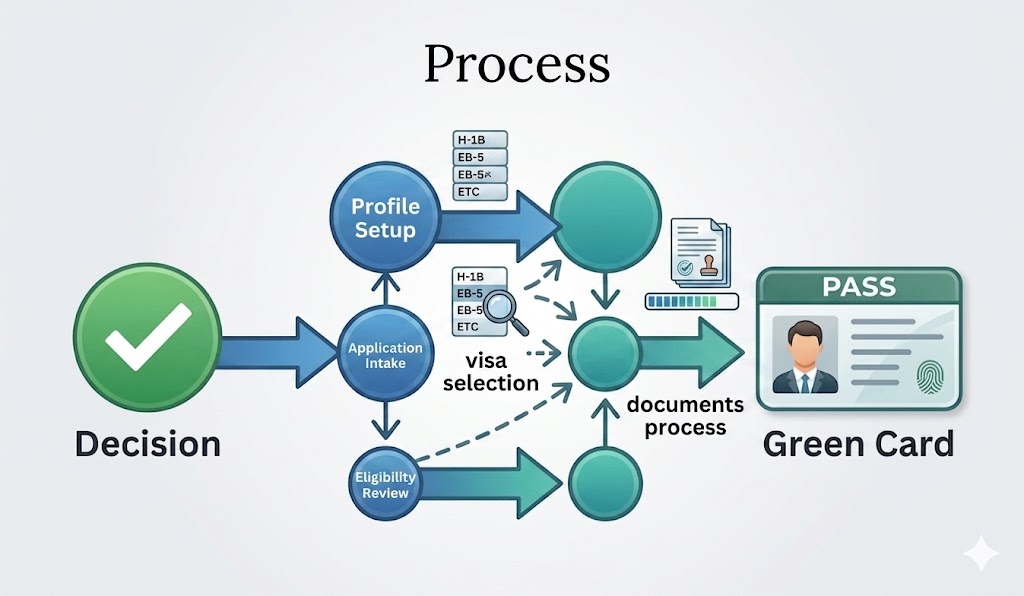

Before you choose a project, before you transfer money, and before you file I-526E, you should understand the full EB-5 process clearly.

EB-5 is not a single application. It is a long journey that includes education, project selection, source-of-funds preparation, subscription, capital transfer, I-526E filing, visa availability, green card application, conditional residence, I-829 filing, and eventually permanent green card approval.

If you only focus on one part, such as the project return or the processing speed, you may miss other risks that can affect your family later.

This article is written to explain what I usually tell investors before they officially begin the EB-5 process.

1. EB-5 is both an immigration process and an investment process

The first thing to understand is that EB-5 has two sides. One side is immigration: the investor wants to qualify for a U.S. green card. The other side is investment: the investor must place capital into a qualifying U.S. commercial enterprise.

USCIS explains that the EB-5 program was created to stimulate the U.S. economy through job creation and capital investment by foreign investors. This means the investment is not just a payment for immigration benefits. The capital must be invested in a way that supports economic activity and job creation.

This is why investors should avoid thinking of EB-5 as simply “buying a green card.” The immigration result depends on whether the investment satisfies EB-5 rules. The investment result depends on project performance, repayment strategy, capital structure, market conditions, and developer execution.

2. The required investment amount is only part of the total cost

Many investors focus first on the required EB-5 investment amount. For petitions filed on or after March 15, 2022, the investment amount is generally $800,000 for a targeted employment area or infrastructure project, and $1,050,000 for other investments.

However, the investment amount is not the total budget. Investors should also prepare for administrative fees, immigration attorney fees, USCIS filing fees, translation and document preparation costs, bank transfer costs, tax advisory fees, and possible travel expenses. If the family plans to move to the United States, they should also consider housing, education, insurance, and living costs.

A smart EB-5 budget should separate three categories: immigration cost, investment capital, and family relocation cost. Investors should not invest all available liquidity into EB-5 without considering future financial needs.

3. Source of funds can take more time than expected

Source of funds is one of the most important parts of the EB-5 process. USCIS must be satisfied that the invested capital came from lawful sources and followed a traceable path to the EB-5 investment.

This can be simple for some investors and complex for others. For example, salary savings may require employment letters, tax records, bank statements, and explanation of accumulated savings. Property sale proceeds may require purchase records, sale agreements, ownership certificates, tax payment proof, and bank records. Business income may require company documents, dividend records, tax filings, audited accounts, and ownership evidence. Gifts and loans require additional documentation to show the original source of the donor’s or lender’s funds.

Investors should start source-of-funds preparation before choosing a project. A project may be ready for subscription, but if the investor’s documents are not ready, filing may be delayed. For families with older records, multiple countries, cash-heavy businesses, crypto assets, or complex family transfers, document preparation may take significant time.

4. Project selection is not only about immigration approval

Many investors ask whether a project has I-956F approval, whether it is rural, whether it has fast processing potential, or whether other investors have already filed. These are important questions, but they are not the only questions.

A good EB-5 project review should include both immigration risk and financial risk. Immigration risk includes job creation, project eligibility, regional center compliance, and document quality. Financial risk includes capital stack, senior loan position, developer equity, construction progress, exit strategy, repayment source, market demand, and sponsor track record.

Investors should understand where EB-5 capital sits in the capital structure. If EB-5 funds are subordinate to senior debt, the repayment risk may be different from a structure where EB-5 capital has stronger collateral or repayment protections. Investors should also understand whether repayment depends on refinancing, sale, operating cash flow, or another capital event.

5. EB-5 timing has several layers

EB-5 timing is often misunderstood. Investors may ask, “How long does EB-5 take?” But there is no single timeline. There are several stages.

First, there is preparation time: choosing a project, preparing source-of-funds documents, signing subscription documents, and transferring funds. Second, there is I-526E processing time. Third, there is visa availability, which depends on the investor’s country of chargeability and the Visa Bulletin. Fourth, there is the green card application stage, either through consular processing or adjustment of status. Fifth, there is the two-year conditional residence period. Finally, the investor must file Form I-829 to remove conditions.

USCIS states that investors file Form I-829 within the 90-day period immediately before the second anniversary of obtaining conditional permanent resident status.

This means EB-5 should be viewed as a multi-year plan, not a quick application.

6. Visa availability can affect your strategy

Even if USCIS approves an I-526E petition, the investor still needs an immigrant visa number to become a conditional permanent resident. The Department of State publishes the Visa Bulletin every month, showing visa availability for different categories and countries.

For countries with high EB-5 demand, backlog can affect the timing of green card issuance. This matters for children close to age 21, families deciding whether to file adjustment of status, and investors comparing reserved and unreserved visa categories.

Investors should review visa availability before filing, especially if they are from countries that may face retrogression.

7. Conditional residence is not the end of the process

Receiving a conditional green card is a major milestone, but it is not the final step. EB-5 investors first receive conditional permanent residence, usually valid for two years. USCIS explains that conditional permanent residents must file to remove the conditions on permanent resident status.

For EB-5 investors, this is done through Form I-829. At this stage, USCIS reviews whether the investment remained compliant and whether the required jobs were created. Investors should continue monitoring the project during the conditional residence period. They should keep communication records, annual reports, tax documents, project updates, and any information relevant to job creation and deployment of funds.

8. You need the right professional team

EB-5 involves immigration law, securities documents, investment review, tax questions, and sometimes cross-border fund transfer issues. A strong professional team may include an immigration attorney, project due diligence advisor, tax advisor, financial advisor, and sometimes a foreign exchange or banking specialist.

Investors should understand the role of each professional. The immigration attorney prepares and files immigration petitions. The project sponsor provides project documents. The regional center may manage EB-5 compliance at the project level. The investor or investor’s advisor should review investment risk. No single party should be expected to cover every issue.

5. How to Set Your EB-5 Goals Before Choosing a Project

One of the biggest mistakes I see among EB-5 investors is choosing a project before clearly defining their goals.

Many investors start by asking:

“Which project is the best?”

But in reality, there is no single “best” project for every investor. A good project for one family may not be suitable for another family. A family with a 20-year-old child may care more about timing and age-out risk. A family with young children may focus more on long-term planning. A business owner may care about relocation flexibility. A conservative investor may focus heavily on repayment structure and capital protection.

That is why I usually ask investors a different question first:

“What are you trying to achieve through EB-5?”

Your EB-5 goals should be clear before you sign subscription documents or transfer investment funds. These goals should cover immigration, family planning, investment risk, source of funds, timeline, lifestyle, and future citizenship planning.

Once your goals are clear, project selection becomes much more logical.

1. Define your immigration goal

The first goal is the immigration goal. Why do you want a U.S. green card?

Some investors want their children to study and work in the United States with more long-term security. Some want to relocate permanently. Some want flexibility to live between countries. Others want to eventually apply for U.S. citizenship.

EB-5 may allow qualifying investors, their spouses, and unmarried children under 21 to apply for lawful permanent residence. But obtaining a green card also creates responsibilities. Permanent residents must consider U.S. residence requirements, tax exposure, travel patterns, and long-term family plans.

If your goal is only short-term travel or temporary stay, EB-5 may not be necessary. If your goal is permanent residence and family flexibility, EB-5 may be more relevant. Your immigration goal should guide every later decision, including filing timing, whether to pursue adjustment of status or consular processing, and whether citizenship is part of the long-term plan.

2. Define your family goal

For many EB-5 investors, the family goal is the real reason behind the investment. The investor may not be planning to move immediately, but the family may want children to attend school in the United States, work after graduation, or have more stable future options.

Family planning should begin with a simple chart: spouse, children, ages, current location, current visa status, education plans, and expected travel patterns. This chart helps identify key risks.

The most important family issue is often children’s age. Unmarried children under 21 may generally be included as derivatives, but families with children close to 21 should analyze age-out risk immediately.

Another family issue is whether all family members want the green card. Sometimes the principal investor does not plan to live in the United States, but the spouse or children do. Sometimes one child is studying in the U.S. while the rest of the family remains abroad. Sometimes the investor wants to preserve flexibility without immediate relocation. Each situation may require a different strategy.

3. Define your timeline goal

EB-5 is a multi-stage process. Investors should separate the timeline into several parts: preparation, I-526E filing, USCIS review, visa availability, green card application, conditional residence, I-829 filing, and permanent green card approval.

The Visa Bulletin is important because visa availability may affect when an investor can move forward to the green card stage. The U.S. Department of State publishes the Visa Bulletin monthly, including Final Action Dates and Dates for Filing.

Some investors need faster immigration timing because a child is near university age or close to turning 21. Others can accept a longer timeline because they are planning for future optionality. Your timeline goal should influence whether you prioritize a reserved visa category, whether you consider rural projects, and how urgently you need to prepare source-of-funds documents.

However, investors should be careful not to choose a project based only on speed. Fast processing is useful only if the project also has strong compliance, job creation, financial structure, and repayment planning.

4. Define your investment goal

EB-5 is an investment, and investment goals matter. Some investors focus on capital preservation. Some focus on repayment timeline. Some focus on project transparency. Some want a lower-risk structure even if the expected return is small. Others are comfortable with more complexity if the immigration benefits appear stronger.

The required investment amount is generally $800,000 for a targeted employment area or qualifying infrastructure project and $1,050,000 for other projects, for petitions filed on or after March 15, 2022.

But investors should not evaluate the investment only by the minimum amount. They should ask:

Where does EB-5 capital sit in the capital stack? Is there senior debt? How much developer equity is in the project? What is the repayment source? Is repayment based on refinance, sale, cash flow, or another exit event? What happens if construction is delayed? What happens if sales or occupancy are weaker than expected? Does the project have enough job creation cushion?

A clear investment goal helps investors avoid being distracted by marketing. If your goal is capital preservation, you should focus on structure, collateral, repayment source, and sponsor track record. If your goal is immigration safety, you should focus heavily on job creation, compliance, project documentation, and I-956F status. Most investors need both.

5. Define your source-of-funds goal

Source-of-funds preparation is not just paperwork. It is a core part of the EB-5 strategy. Investors should identify the cleanest and most documentable source of capital before transferring funds.

A common mistake is choosing the most convenient money instead of the most documentable money. For example, funds may be available in one account, but the history may be difficult to explain. Another asset, such as property sale proceeds or salary savings, may be easier to document even if it requires more preparation.

Your goal should be to create a clear, logical, and well-supported source-of-funds story. USCIS should be able to understand where the money came from, how it was earned, how it moved, and how it reached the EB-5 investment.

6. Define your U.S. lifestyle goal

A green card is not only an immigration document. It affects lifestyle. Investors should think about whether they plan to live in the United States full-time, part-time, or only in the future.

If you plan to move permanently, you should consider housing, school districts, health insurance, tax planning, business ownership, and family adaptation. If you plan to travel frequently, you should understand the rules for maintaining permanent residence. If you plan to eventually apply for citizenship, travel history and physical presence become even more important.

EB-5 investors receive conditional permanent residence first, and later must file Form I-829 to remove conditions. USCIS states that Form I-829 should be filed within the 90-day period before the second anniversary of obtaining conditional permanent resident status.

This means your lifestyle goal should also align with your I-829 timeline and long-term residence plan.

7. Build your EB-5 goal statement

Before choosing a project, investors should write a simple goal statement. For example:

“Our goal is to obtain U.S. permanent residence for both parents and two children, prioritize immigration safety and job creation, avoid age-out risk for our older child, maintain reasonable capital protection, and keep the option of U.S. citizenship open in the future.”

This kind of statement helps guide every decision. If a project is fast but financially weak, it may not match the goal. If a project is financially strong but has weak job creation, it may not match the goal. If a filing strategy creates risk for a child close to 21, it may not match the goal.

8. Final thought

The EB-5 process becomes much clearer when investors define their goals early. Immigration, investment, timeline, family, source of funds, and lifestyle should all be reviewed before selecting a project.