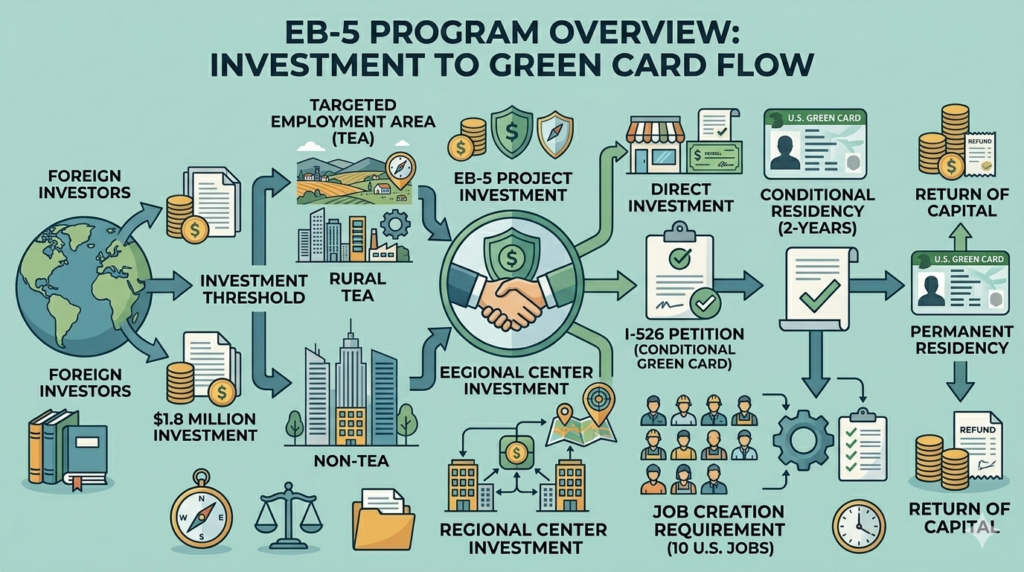

EB-5 is a U.S. immigrant investor visa category that allows qualified foreign investors and eligible family members to apply for U.S. permanent residence through investment in a job-creating U.S. business.

The name “EB-5” comes from Employment-Based Fifth Preference, which means it is the fifth preference category under U.S. employment-based immigration. Unlike temporary visas, EB-5 is designed as a pathway to a U.S. green card.

At its core, EB-5 has three major requirements. First, the investor must invest the required amount of capital into a qualifying U.S. commercial enterprise. Second, the capital must generally be placed at risk, meaning it must be actively used for business activity rather than simply kept in a passive or guaranteed account. Third, the investment must create at least 10 full-time jobs for qualified U.S. workers.

For investors, EB-5 is not only an immigration process. It is also a financial decision. A good EB-5 investor should understand both sides: the immigration requirements and the investment risks. Getting a green card depends on satisfying USCIS rules, while getting money back depends on the project’s financial performance and exit strategy.

There are two common ways to invest: through a regional center project or through a direct EB-5 business. Regional center projects are usually more passive and may count indirect job creation. Direct EB-5 investments usually require a more active business role and rely mainly on direct employees.

EB-5 can be suitable for families who want long-term U.S. residence, access to U.S. education, more flexibility in employment, and a potential path to citizenship. However, it is not a simple “buy a green card” program. Investors must prove lawful source of funds, follow strict filing procedures, and accept that both immigration and financial results involve risk.